Update 1/11/2024:

The specific practice loan that I referenced as giving rise to this post began earlier in 2023, and this post was months in finalizing. I’d originally intended to publish it in the summer. Since publishing, I’ve since learned that RP’s extra support has briefly paused.

That’s right, at least for a month or two, the group’s compensation reached the threshold that turned off the “advance” from RP. Hospital subsidies saved the day. Note that the loan term itself isn’t over, and after briefly not needing it, the group has since required more gravy.

Ultimately, this suggests that RP may have chosen the loan method for supporting this practice because they had specific reasons to (correctly?) believe that the loan period would be time-limited: It’s obviously better to give some money temporarily in a non-binding fashion to save a group in crisis than to permanently change the contract if you don’t have to.

The real question for the future will be: will the group consistently earn enough in the end to pay back several million dollars of borrowed money, and if so, how long does that take? And/or, does the group fight it? It sounds like what seemed like free money at the time may ultimately be an actual loan, and paying back that advance will therefore constrain compensation going forward unless long-term profits stay below the mark due to increased contractor use, the need to sweeten up internal moonlighting rates, or understaffing requires dropping volumes. Any or all of those things may happen. They are things happening at groups of all stripes across the country.

The future remains uncertain as always—and RP may still never recoup this loan—but this also means that I was wrong in how easily I dismissed the likelihood of RP seeing some of this money back.

This month credit agency Moody’s downgraded Radiology Partners again (surprising exactly no one): the first (and smallest) of its large debt obligations is due in 2024, they currently owe 10x their earnings, and they can only service these debt obligations through refinancing, which is challenging in the current market even before you consider the potentially tenous state of RP’s acquired practices when they reach their 5-year vesting window. It was inevitable.

If you ask RP, they will tell you that all third parties—whether Moody’s or just a random internet troll like myself—don’t understand their business and aren’t privy to the magic happening behind the scenes.

They consistently maintain that they will be able to refinance, though they never publically acknowledge that the most likely refinancing they will achieve is some form of distressed exchange like a debt-to-equity swap that would likely dilute current shareholders (and is considered a bankruptcy equivalent).

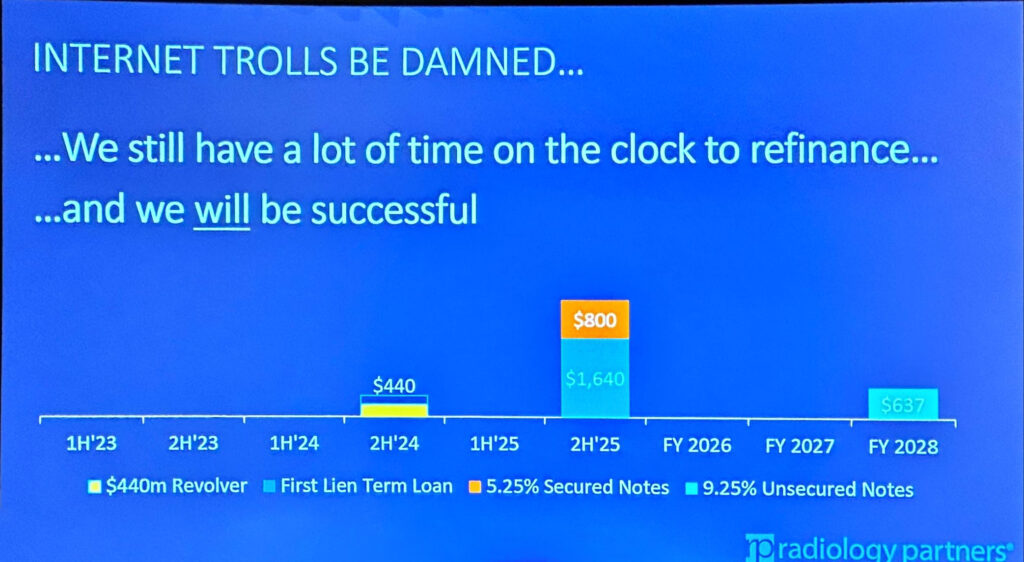

Here’s a slide from their big meeting earlier this year:

I know some people in the radiology community think that when the debts come due that RP will go bankrupt and disappear, but that’s simply not going to happen. Depending on how broadly one defines “success,” there’s an excellent chance they’ll be successful. (To wit, Envision emerged from bankruptcy in the hands of its creditors, but it didn’t go anywhere.)

But here is something you haven’t seen in the news but is nonetheless interesting:

Radiology Partners—already dealing with recurrent credit downgrades, cashflow problems, and investor fears—has been offering no-interest loans to some of its practices to shore up compensation.

Note: I’ve heard a similar story independently from several RP radiologists, but I do not know how common the offer has been (I suspect not very). For what it’s worth, I did reach out to RP and Melinda Collins (AVP of Marketing and Communications) on Twitter/X last week without a response. If you’re at RP and want to weigh in on this purported practice, please reach out. If I’m wrong or misleading in any way, I really, really want to know.

To my knowledge, nobody has pressed RP on this issue yet, and it has not been discussed in any public forum other than a brief mention on this site earlier this year in a quotation from a former RP radiologist. Since that time, I heard from multiple sources that at least one practice has taken the offer, hence this post.

So how does this look in practice? Let’s discuss.

Read More →